Semiconductor Weakness Turns Into a Global Correction as Japan Absorbs Heavy Selling Pressure

Despite sharp price declines, underlying AI spending from hyperscalers remains elevated, supporting the longer-term structural case for the sector.

None of this is financial advice. Do your own research. By reading this newsletter, you acknowledge and accept the terms and conditions outlined in our disclaimer.

GM Investors,

In our analysis, the semiconductor sector is experiencing something more significant than a typical correction. After a powerful multi-year rally, investors are rapidly reassessing valuations, pushing the SOX Index down nearly 19% from its recent peak. What stands out to us is that this move appears driven more by sentiment than by any major breakdown in underlying fundamentals.

The impact of this semiconductor weakness has extended well beyond the United States. With South Korea’s market closed for a holiday, much of the selling pressure shifted toward Japan, creating an uneven but intense regional reaction. In a single session, Asian markets saw over $970 billion wiped out, with Japan alone losing $350 billion as the Nikkei entered a technical correction. This rapid spillover highlights how interconnected global semiconductor sentiment has become.

While today's declines are notable, we believe this is a classic case of sector rotation rather than a general risk-off event. Capital appears to be shifting away from names that have rallied significantly and toward areas that have lagged. The S&P 500 has remained resilient despite a sharp correction in semiconductor stocks, reinforcing our belief that this is more of a reallocation within equities than widespread market fear. Stable hyperscaler AI spending could improve conditions in the year’s second half by normalizing valuations.

While macro stays heavy, the FIFA World Cup is offering a fun way to stay active in markets ⚽️🏆!!!

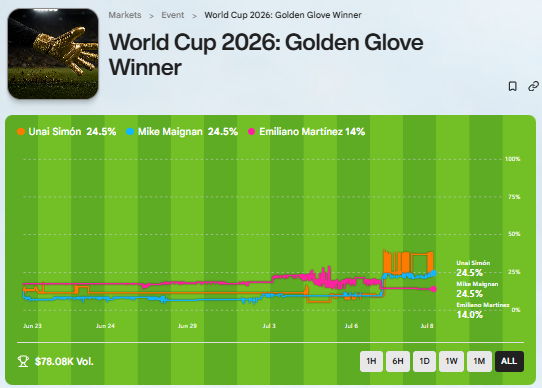

Golden Glove Race Heating Up on Rain Trade Markets

With the knockout stages producing dramatic clean sheets and penalty shootout heroics, the Golden Glove is trading dead even, Unai Simón at 24.5%, Mike Maignan at 24.5%, with Emiliano Martínez at 14% on Rain Trade. The market has tightened sharply after Martínez’s quarterfinal masterclass, but short-term swings around upcoming semifinal matchups often create trading opportunities.

Here’s what we’re watching:

Simón’s shot-stopping and distribution make him the live favourite in a Spain side that dominates possession

Maignan’s penalty-saving pedigree can move the market quickly in these fixtures as he was the hero vs. England

Martínez’s mind games and clutch saves have flipped this market before; never count him out

Short-term football markets offer fast execution during quieter crypto periods

Rain Trade continues to see strong volume on these international matches with clean order flow and tight spreads.

📻 Sneak Peak Recording

HYPE Spot Movements & VC Wallet Hopping → On-Chain Speculation: The team analyzed the weak relative performance of the Hyperliquid token (HYPE), noting that while on-chain alerts revealed $25 to $28 million being moved by Andreessen Horowitz through a16z wallets.

The $970 Billion Tech Wipeout as Japan is absorbing the Semis selling pressure

In our analysis, what began as semiconductor weakness in the U.S. has now evolved into a global correction, with Asian markets absorbing significant selling pressure today. With South Korea’s market closed for a holiday, Japan became the primary destination for the selling. Asian equities saw over $970 billion wiped out in a single session, with Japan alone losing $350 billion (51 trillion yen) as the Nikkei fell sharply and entered a technical correction.

The speed of today’s move highlights how interconnected semiconductor sentiment has become across regions. Japanese technology stocks, including Tokyo Electron and Advantest, were among the hardest hit, falling more than 9-10% in recent sessions. Back in the U.S., the SOX Index has now fallen 19% from its June all-time high, placing the sector on the verge of a technical bear market. Many AI infrastructure and memory stocks have also dropped between 20-40% from their recent peaks in just a few weeks.

The speed of today’s move in Japan highlights how interconnected semiconductor sentiment has become across regions. When one major market remains shut, liquidity and selling pressure tend to concentrate elsewhere. Japanese technology stocks, including Tokyo Electron and Advantest, were among the hardest hit, falling more than 9-10% in recent sessions. This uneven regional impact turned Japan into the focal point of today’s global semiconductor selloff.

This appears to be a classic case of positioning and sector rotation rather than a broad-based risk-off move. After many semiconductor names rallied 4-5x over the past year, investors are taking profits and shifting capital toward areas that have lagged, such as SaaS and parts of the Magnificent 7. The S&P 500 has remained near record highs even as semis corrected sharply, reinforcing our view that this is a reallocation within equities rather than widespread fear.

Despite the sharp price action, underlying fundamentals remain resilient. TSMC delivered strong second-quarter results with profits rising 77% year-over-year, while ASML also reported solid numbers. Hyperscalers continue to guide for elevated AI-related capital spending in the coming years. Recent analysis on memory markets suggests that while near-term pricing may peak around 4Q26, the broader cycle has the potential to extend rather than collapse.

The pain has been particularly acute in memory and storage names. Dell, Western Digital, Seagate, and Micron have led the recent decline. Comments from ASML about high-end tools improving memory performance, combined with increased competition from Chinese players, added to the pressure. Following the selloff, many of these stocks now trade at significantly lower valuations, which may attract longer-term buyers if earnings remain strong.

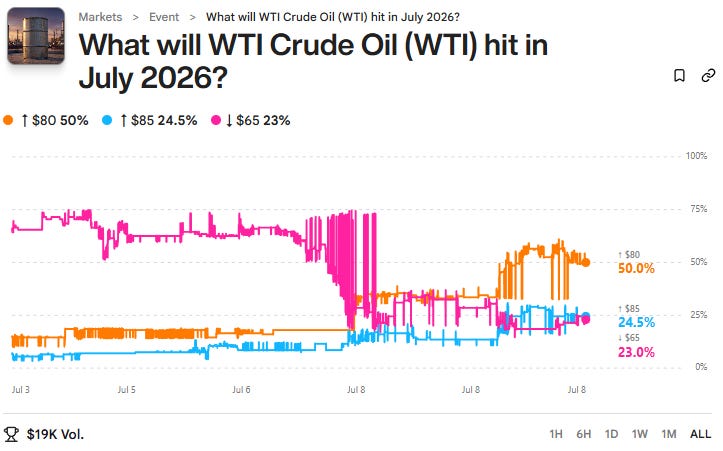

WTI Crude Oil Heating Up on Rain Trade Markets

With Middle East supply disruptions sending shockwaves through global energy markets, WTI is trading at 50% to hit $80 as the highest daily closing price in July 2026 on Rain Trade, with $85 at 24.5% and $65 at 23%. The market has flipped dramatically after the latest escalation, but short-term swings around ceasefire headlines and SPR release rumors often create trading opportunities.

Here’s what we’re watching:

Geopolitical risk premium is back in the barrel, any supply disruption headline moves this market 10-15% in minutes

SPR release rumors can flip the market quickly in these fixtures.

$80 as the new floor, the chart shows a violent repricing from $65 dominance to $80 as the clear favourite

Short-term commodity markets offer fast execution during quieter crypto periods

Rain Trade continues to see strong volume on these high-profile macro events with clean order flow and tight spreads.

Rain Trade

U.S. Semiconductor Reset Creates Opportunity Amid Strong Fundamentals

In our analysis, the sharp correction in U.S. semiconductor stocks appears to be driven more by sentiment and positioning than by any major breakdown in fundamentals. Memory and storage names have been among the hardest hit, with Dell, Western Digital, Seagate, and Micron leading the decline in recent weeks. The selloff has pushed many of these stocks down 20-45% from their recent highs.

Recent analysis on memory markets indicates that DRAM contract prices are rolling over from cyclical peaks. Pricing is expected to peak around 4Q26, after which the rate of growth is likely to moderate. At the same time, valuations (measured by next twelve months price-to-book) have yet to fully re-rate lower. This suggests that while near-term memory pricing may face pressure, the broader cycle still carries the potential to extend rather than collapse abruptly.

Despite the weak price action, underlying demand remains positive. Micron expects profits that exceed its lifetime performance, and hyperscalers continue to forecast increased AI-related capital spending in the coming years. The current weakness in memory stocks appears to be the result of short-term positioning adjustments rather than a structural decline in AI-driven demand.

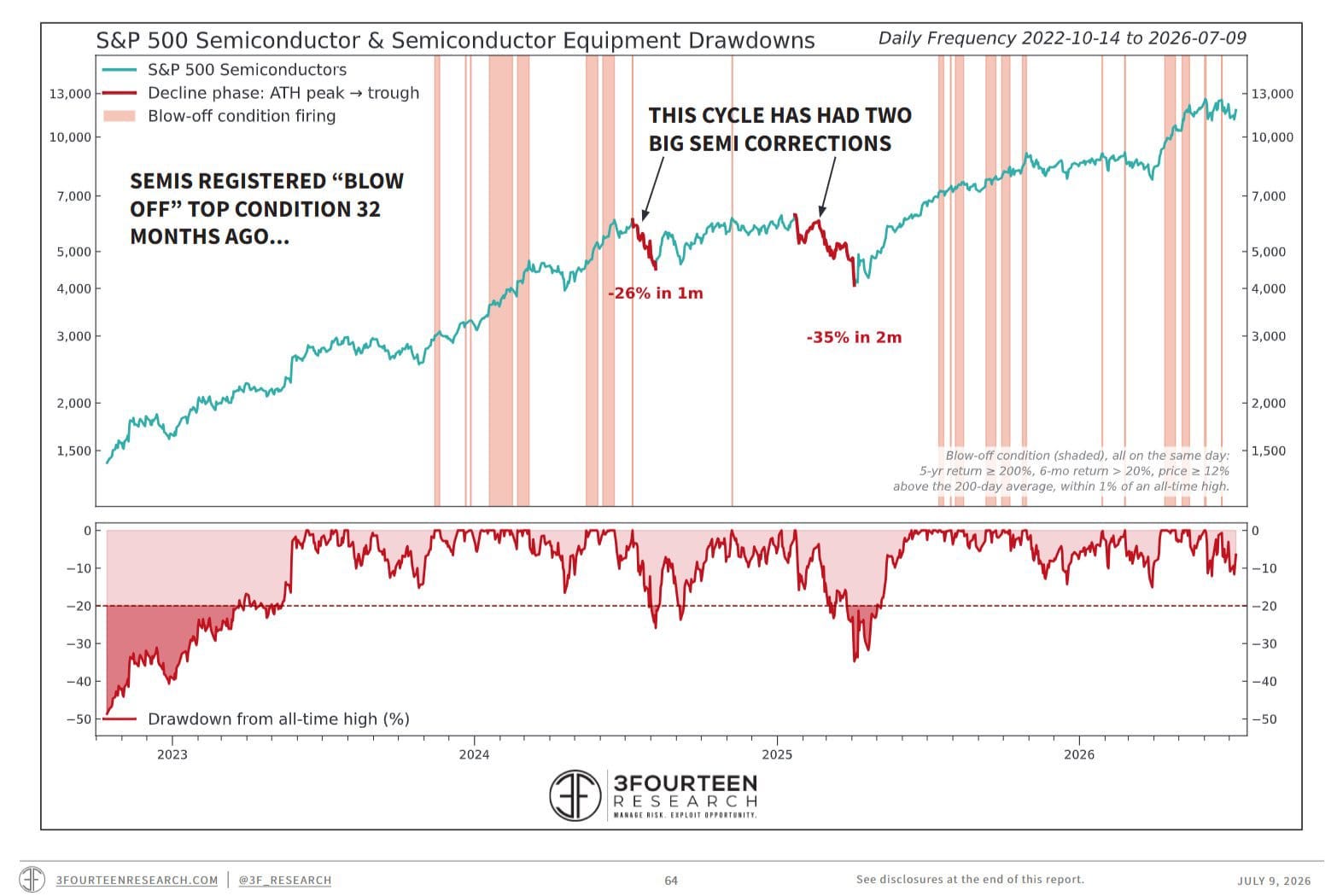

History shows that semiconductor sectors often go through sharp sentiment resets during bull markets. Semiconductor stocks first flashed a “blow-off” signal roughly 32 months ago and have already survived two separate 20%+ corrections in this cycle before making new highs. While every period is different, past resets have frequently created better entry points when the long-term demand thesis remained intact.

In our view, the current correction may represent another mid-cycle reset rather than the end of the AI infrastructure theme. Many memory stocks now trade at significantly lower valuations following the selloff, which could attract longer-term buyers if earnings remain supportive. With semiconductor stocks comprising close to 20% of the S&P 500, continued strength in hyperscaler capital spending could create a more favorable setup in the second half of the year.

Yesterday, semiconductor weakness persisted and spread more visibly into Asian markets. Today, volatility is expected to remain elevated. We are also monitoring currency markets, where yen shorts have reached near-record levels, raising the possibility of surprise intervention by the Bank of Japan. Key developments to watch include upcoming memory company updates and any fresh signals on hyperscaler spending plans. If long-term AI demand fundamentals hold up, this type of sharp correction can often mark a short-term bottoming process.

Poll of the Day (Powered by Rain Trade) 🎯

🌍 Market Catch-Up

Top 100 coins Daily Performance - Banter Bubbles

bearish cryptocurrency market, characterized by an overwhelming sea of red as major assets like BTC and ETH experience notable losses. However, a few distinct green outliers, such as PI and CRO, are bucking the prevailing downward trend to demonstrate strong positive momentum.

🐸 MEMEoirs of a Degen!

💭 Banter’s Take

In our opinion, what we are seeing right now is not the breakdown of the AI trade but rather a sharp and overdue sentiment reset. After years of aggressive positioning in semiconductor and AI-related stocks, the market is simply reaping profits and shifting capital to areas that have fallen behind. The fundamentals of AI spending have not deteriorated; if anything, they remain positive.

The speed and scale of the move in both the US and Asian markets demonstrate how crowded the trade had become. When sentiment shifts quickly, even strong companies and industries can become caught in the crossfire. We've seen this pattern before in this cycle, and history shows that these types of resets often result in better risk-reward setups rather than signaling the end of an uptrend.

Nonetheless, near-term volatility is likely to remain elevated. We'll be paying close attention to how chip stocks perform in the coming sessions, particularly whether oversold names can find support and whether hyperscaler spending commentary remains strong. For the time being, we see this as a healthy rebalancing of the overall market rather than a structural shift in the AI narrative.

Stay sharp.

In an environment where political noise is high but actual liquidity and conviction remain low, having the right execution tools matters more than ever. That’s why we’ve partnered with Rain Trade; a platform built for traders who need speed, precision, and clean betting odds in volatile conditions like these.

None of this is financial advice.

Do your own research.

As a valued subscriber to Good Morning Crypto, you are part of the wider Crypto Banter ecosystem - and that means you get first access to something we’ve been building behind the scenes. We’re thrilled to announce the launch of The Insider, Crypto Banter’s brand new publication designed to give our community a deeper, closer look at everything happening across our network. As an existing Good Morning Crypto reader, you’ve been added to The Insider as part of our founding subscriber rollout. You’ll continue to receive Good Morning Crypto as normal - The Insider is an exciting addition to your inbox, not a replacement.